As older adults look toward retirement, financial stability becomes a top priority, especially for those living on fixed incomes. One lesser known, yet potentially helpful, option is the reverse mortgage.

While it may not be the right fit for everyone, a reverse mortgage can provide flexibility and peace of mind by turning home equity into usable income. In this guide, we’ll walk you through what reverse mortgages are, how they work, the different types available, and whether this option might be a good fit for your needs.

What Is a Reverse Home Mortgage?

A reverse mortgage is a loan that allows homeowners ages 62 and older to turn a portion of their home’s equity into cash. Unlike a traditional mortgage, where you make monthly payments to a lender, with a reverse mortgage, the lender pays you. You can receive this money in a lump sum, as monthly payments, or as a line of credit to use when needed.

One of the biggest appeals is that you don’t have to repay the loan as long as you live in the home. Instead, the loan is paid back when you sell the home, move out permanently, or pass away. At that point, the proceeds from the home’s sale go toward paying off the loan, and any remaining value belongs to you or your heirs.

Reverse mortgages are more common than many realize. Nearly 33,000 Home Equity Conversion Mortgages (HECMs) were endorsed in the U.S. in 2023 alone.

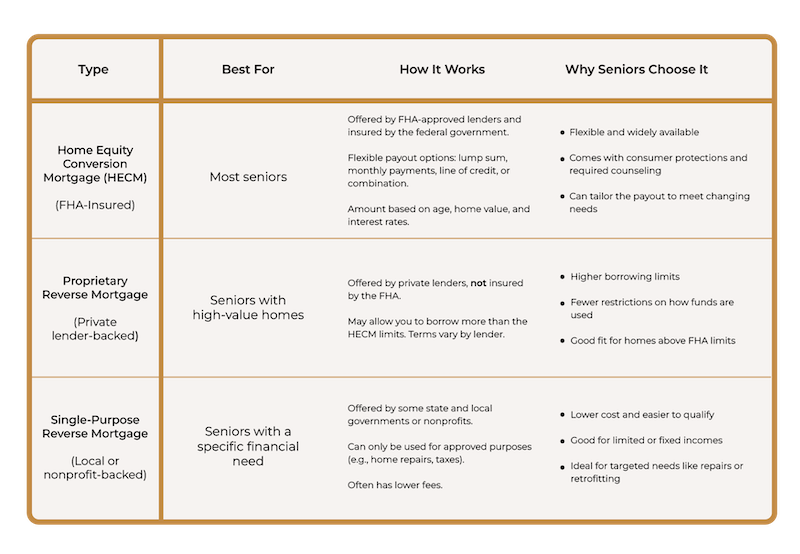

Types of Reverse Mortgages

There are three main types of reverse mortgages:

To qualify, seniors must:

- Be at least 62 years old

- Own their home outright or have a low remaining mortgage balance

- Live in the home as their primary residence

- Stay current on property taxes, homeowners' insurance, and maintenance

- Attend a HUD-approved counseling session

For more requirements, read here.

When and How to Use a Reverse Mortgage

Reverse mortgages are often most useful for seniors who plan to remain in their homes for many years. They can be used to boost monthly income, eliminate an existing mortgage payment, fund in-home care, or delay drawing from other retirement accounts—helping those accounts continue to grow.

According to a 2024 AARP survey, more than 70% of seniors prefer to “age in place” in their own homes rather than relocate. A reverse mortgage can help make that possible by turning a home into a financial asset while staying in familiar surroundings.

The funds can be received in different ways based on your preferences: a lump sum for larger needs, fixed monthly payments for stability, or a line of credit for unexpected expenses down the road. Some borrowers even choose a combination of these.

Pros and Cons of Reverse Home Mortgages

Like any financial tool, a reverse mortgage has both benefits and drawbacks.

On the positive side, it provides a source of tax-free income without requiring you to sell your home. That can be a lifeline for covering everyday expenses, home modifications, medical care, or simply enjoying retirement more comfortably. Since you remain the owner of your home, you can age in place with greater independence.

However, there are trade-offs. Because you’re not making payments, the loan balance grows over time due to interest. This can reduce how much equity is left for your heirs. There are also upfront costs, including origination fees and mortgage insurance. And if you move out of the home—even into assisted living or a nursing facility—the loan may become due.

Is This the Right Fit for You?

A reverse mortgage isn’t for everyone, but for the right homeowner, it can be a powerful tool. If you're looking to stay in your home and want to improve your cash flow without adding monthly bills, it might be worth considering. It may also be a good fit if you don’t have plans to leave your home to heirs, or if you’re already looking at ways to fund care or maintain your lifestyle in retirement.

On the other hand, if you're planning to move soon, if your spouse isn't listed on the mortgage, or if passing your home down is important to you, this might not be the ideal choice. As always, consulting with a financial advisor or counselor can help you weigh your options with confidence.

How Repayment Works

Repayment is one of the most important—and often misunderstood—parts of a reverse mortgage. Unlike traditional loans, a reverse mortgage doesn’t require monthly payments. Instead, the loan becomes due when the homeowner sells the house, moves out permanently, or passes away.

At that point, the home is typically sold, and the proceeds are used to pay off the loan balance, which includes the borrowed amount, interest, and fees. If the sale of the home exceeds the loan balance, the remaining equity belongs to the homeowner or their heirs.

Importantly, reverse mortgages are non-recourse loans, meaning you or your heirs will never owe more than the home is worth, even if the loan balance ends up exceeding the property’s value. This offers an added layer of protection for families navigating the repayment process.

Questions to Ask Before Getting a Reverse Mortgage

If you’re considering a reverse mortgage, asking the right questions can help you make a more confident decision. Here are a few to start with:

- Do I plan to live in this home for the foreseeable future (5+ years)?

- Can I afford to keep up with property taxes, insurance, and maintenance?

- How will this affect my estate or any inheritance I hope to leave behind?

- Have I talked to my family or financial advisor about this decision?

- Have I completed a counseling session with a HUD-approved counselor?

- Am I comfortable with the loan balance increasing over time?

Thinking through these questions and discussing them with trusted loved ones can bring clarity to whether this option aligns with your long-term goals.

Alternatives to Reverse Mortgages

A reverse mortgage isn’t the only way to access financial support in retirement. If it doesn’t feel like the right fit, consider these alternatives:

- Downsizing: Selling your current home and moving to a smaller or more affordable property can free up cash and reduce living expenses.

- Home Equity Loan or HELOC: If you have strong credit and income, these options let you borrow against home equity, though they do require monthly payments.

- Renting: Selling your home and renting can reduce the responsibilities of ownership while unlocking equity.

- Government or nonprofit programs: Some local or state agencies offer property tax relief, utility assistance, or home repair grants for older adults.

- Living with family: Multigenerational living can be both financially and emotionally rewarding for some families.

Exploring all your options ensures you choose the solution that fits your lifestyle, goals, and financial needs.

Final Thoughts

A reverse mortgage can be a smart way to make the most of your home’s value while still living in it. Even though it’s not without complexity, it offers a practical path forward for seniors who want to access extra funds and stay in familiar surroundings.

Still have questions? Talk to a trusted financial professional to see how a reverse mortgage could fit into your future.